SHI Update 5/17/17: We’re Number 1!

SHI Update 5/10/17: Flying High

May 10, 2017

SHI Update 5/24/17: The FED and the Steak House

May 24, 2017

Who is the world’s largest oil producer?

It may soon be the US.

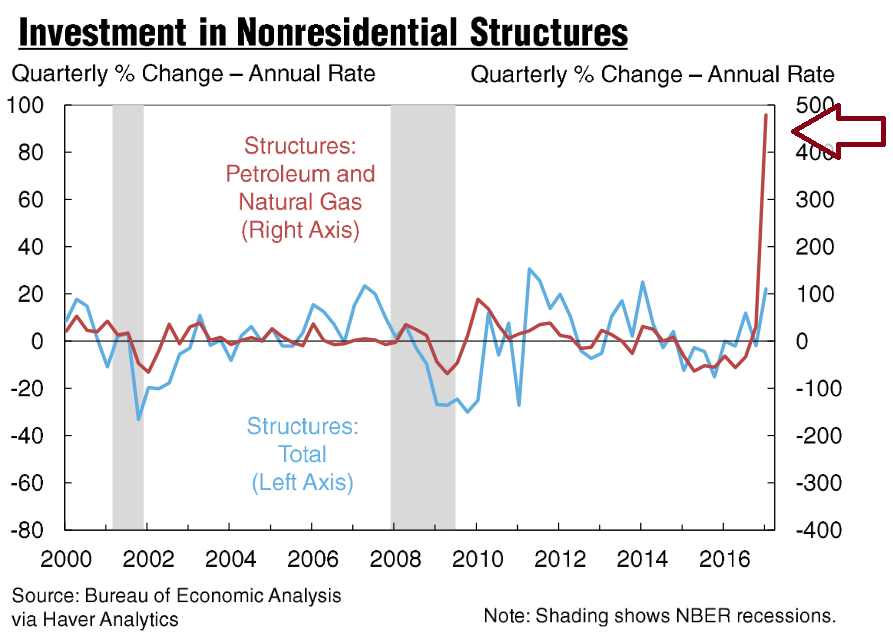

OPEC, and non-member Russia, are cutting production in an effort to maintain current prices. At the same time, US shale producers have invested a staggering amount of new capital into US production. Check out this chart, courtesy of the Federal Reserve Bank of NY:

The red line shows changes in US investment in oil and gas structures over time. It’s pretty easy to see the massive spike in ‘new structures’ at the end of 2016.

US oil production peaked at 9.61 million barrels-per-day (MBPD) in June of 2015, but slipped to 8.5 MBPD last summer. Today, the US EIA is forecasting US production to average about 10 MBPD for the next year.

Currently, Russia is number one at 10.3 MBPD, with Saudi Arabia a close 2nd at 9.95 MBPD. But as they cut … and we increase … it’s likely we will become #1 by 2018. Isn’t that a kick!

You probably have a few questions, perhaps:

- What does this mean for the US economy?

- Will this affect the price of USDA Prime beef?

- Should I buy a camel?

These questions – and more! – will be answered today! 🙂

Welcome to this week’s Steak House Index update.As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/)

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been true for decades…and notwithstanding plenty of predictions to the contrary, it will continue to play this role for years to come. Fear not.

Nominal global GDP is about $76 trillion. US GDP is almost $19 trillion. Is it growing or shrinking? If it’s growing … how rapidly? How might this information impact our daily financial and business decisions?

The objective of the SHI is simple: To predict the GDP direction ahead of official economic releases. While the objective is simple, the task is not. BEA publishes GDP figures the instant they’re available. Unfortunately, the data is old, old news; it’s a lagging indicator.

‘Personal consumption expenditures,’ or PCE, is the single largest component of the GDP. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early. Not when it’s too late.

Taking action: Keep up with this weekly BLOG update. If the SHI index moves appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG: Sure, I too could comment on President Trumps latest (insert your own adjective and noun). But I won’t. Except to this extent: Today, the DJIA, S&P and Nasadaq are not happy. Not at all. Clearly, the markets are concerned the Trump administration agenda of tax cuts and infrastructure spending are at risk.

But on the other side of the ledger, the US is on the verge of becoming the leading global oil producer! Which, ironically, will probably have a depressing effect on oil prices. Remember: Oil is a global commodity. At present, the most important commodity on the planet. Global distribution systems are very efficient which means the supply/demand relationship is highly correlated with current prices.

Yes, OPEC and Russia plan to cut production. But it looks likely the US will replace any shortfall. Thus, global supply – if affected at all – should remain consistent.

Demand is also fairly consistent. Demand growth has been kept in check by consistently increasing alternative energy production and relatively slow global economic growth.

Meaning the price of oil is unlikely to increase much, if at all. As energy is one of the largest components of the CPI and PCE, US inflation, too, will remain tame.

No, don’t buy a camel. They can be surly. 🙂

What are the SHI and ‘Steakonomics’ telling us this week? Once again, if our absurdly expensive steak houses are an accurate barometer, the consumer spending component of our GDP appears to be safe for another week. With the one consistent exception, our restaurants are well booked:

As you can see, conditions were similar one year ago. This week last year, Mastros was fully booked. This week, Morton’s has that honor. Both SHI readings are fairly close.

I’ve slightly reformatted the SHI trend report. As you’ll see below, I’ve redone the “conditional formating” to ensure the color scale accurately shows the highs (green) and lows (red.)

Next week, I plan to do a bit more reformatting. I will change the appearance to permit a side-by-side comparison of 2016 against 2017. I think you will like the change. Here is this week’s SHI trend report:

Let me finish with this comment.

One could easily worry about the current economic expansion. Now 95 months old, it is the 3rd longest in US history going back to 1854.

But expansions don’t die from old age. Typically, some exogenous adverse event shocks the economy into recession. Rest assured, there are plenty of potential bear traps out there. Just none that scare me (too much) right now.

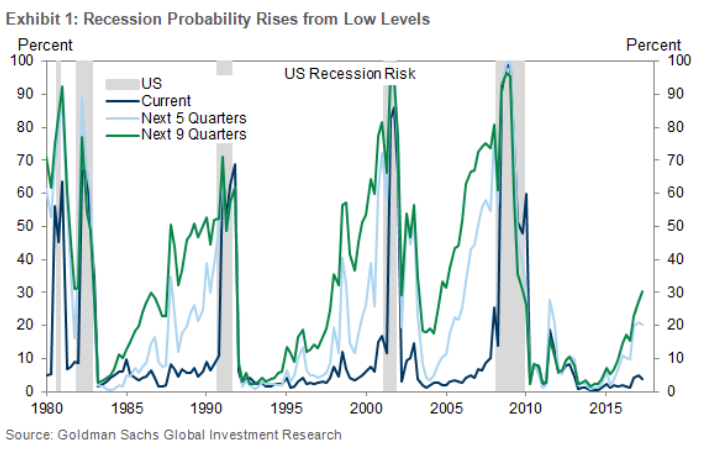

Goldman Sachs agrees:

Goldman puts the odds of a recession within the next few years (9 quarters) at only 31%. Further, they feel there’s a better than 2/3 chance our current economic recovery will become the longest US recovery ever! Another number 1!

We’ll keep watching for bear traps. But for now, rest easy. All is well.

- Terry Liebman

2 Comments

Hey very nice site!! Man .. Beautiful .. Amazing .. I will bookmark your blog and take the feeds also…I am happy to find numerous useful info here in the post, we need develop more techniques in this regard, thanks for sharing. . . . . .

Very good blog. Much obliged.