SHI Update 6/7/17: Liars Poker

SHI Update 5/31/17: R-Words

May 31, 2017SHI Update 6/14/17: Point to the Future!

June 14, 2017

“There are three kinds of lies: lies, damned lies, and statistics.”

A very funny quote, whether originally uttered by Mark Twain, a humorist, or Samuel Disraeli, a politician. And perhaps even a bit accurate.

Today, if either of these gentlemen were to repeat the comment, I suspect they would be referring to statistics from the BLS, specifically those in “The Employment Situation.” Because the numbers behind the numbers tell a very different story than the very exciting “4.3% unemployment” statistic in last Friday’s press release. Very different.

Welcome to this week’s Steak House Index update.As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/)

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. Is it expanding or contracting?

Nominal global GDP is about $76 trillion. US GDP is almost $19 trillion. Is it growing or shrinking? If it’s growing … how rapidly? How might this information impact our daily financial and business decisions?

The objective of the SHI is simple: To predict the GDP direction ahead of official economic releases. While the objective is simple, the task is not. BEA publishes GDP figures the instant they’re available. Unfortunately, the data is old, old news; it’s a lagging indicator.

‘Personal consumption expenditures,’ or PCE, is the single largest component of the GDP. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early. Not when it’s too late.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

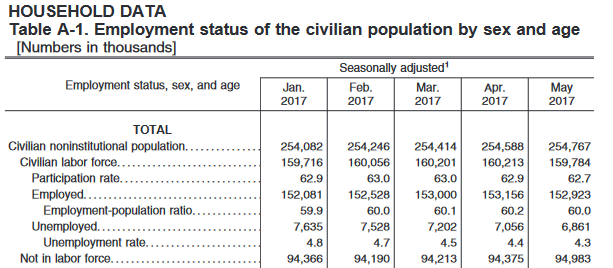

The “numbers behind the numbers” are worth disecting. Because while the headline 4.3% unemployment rate is definitely exciting – and worth trumpeting – it doesn’t tell the whole employment story.

Each month, our US population increases. The rate of that increase is slower today than in the past, but growth remains positive. And each month, the “civilian non-institutional population” (folks 16 or over who are not in prison or otherwise unable to work) increases as well. Last month by 179,000 folks.

With both population and the number of hardy, 16+ year-olds ready for opportunity increasing each month, we would expect the size of the labor force to do the same. Right? Wrong.

At the same time the unemployment rate fell to 4.3%, the “civilian labor force” declined. In fact, as you can see below, the number of folks “not in the labor force” increased by 617,000 since January of this year. And the number of people actually employed decreased by about 233,000.

Which defies logic. With a declining unemployment rate, we would expect the number of people employed to be increasing. It is not.

The bottom line: Yes, it’s great to see a 4.3% unemployment rate. But when this number is the result of more people leaving the labor force than actually getting jobs, the statistic becomes suspect. And a bit misleading.

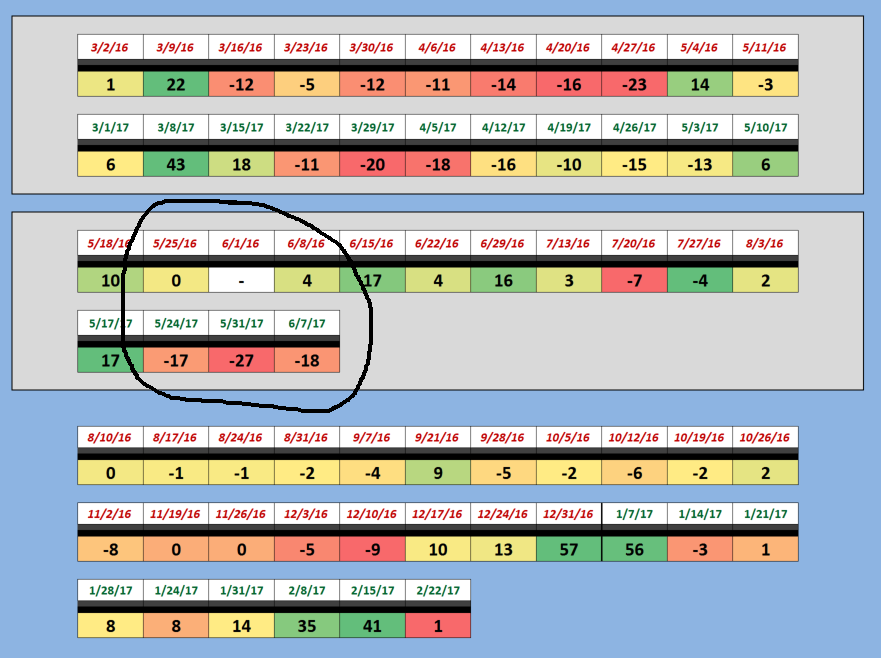

Ruth’s Chris Steak House in Irvine, however, assures us they’re genuine. Nothing suspect here! We’re assured they serve “the finest USDA Prime beef available, broiled at 1,800° and served on 500° plates, so your steak stays hot, juicy and delicious from first bite to last.” Sounds good to me! But their table booking statistics are not quite as robust:

Yet again, the SHI is showing continued weakness. Comparing today’s SHI to one year ago, Mastro’s popularity is about the same … but our other three extravagant eateries seem to be struggling to book tables for this Saturday. With the exception of the 6:30 time slot, this Saturday every slot is open at Ruth’s Chris, Mortons and the Capital Grille. Last year, this week, conditions were very different.

In fact, last year conditions were significantly better for the previous 3 weeks:

Am I ready to pronounce this economic expansion is over? Because consumer spending seems to be tapering off?

Not yet. But I’m leaning in that direction. Slightly. The recent SHI numbers are definitely concerning. And if they continue to show weakness, I may soon change my tune and declare our economic expansion may soon become a contraction. Not yet.

But the FED meets next week and there’s talk of yet another rate 25 basis point increase. While I don’t believe a rate increase is warranted now, the FED may disagree, deciding the time is right as they work to “normalize” the FED funds rate.

Could this move be the straw that breaks the US economic camel’s back? Let’s see what next week brings.

- Terry Liebman

2 Comments

Dear Terry,

As an avid follower of the steak house index and a disciple of his highness Willie, I have read the blog religiously since it’s inception. I appreciate your wisdom and the speculation you bestow upon us. That being said, I throw the metaphorical guantlet down in front of you. Make a decision and take a gamble. Do away with the “let’s see what happens next week”, the “it MAY be forecasting…”, and the “these may be threatening storm clouds”. I want a hard decision. What is the economy going to do? I come to you looking for answers in a time where all news outlets spell nothing but trouble.

Don’t be the economist we want, be the economist we need!

Sincerely,

Your steak house disciple

A disciple! Thank you! I’m so happy! 🙂

First, thanks for the comment. I wish more readers would do the same. Look: I, too, want hard decisions – but sometimes the data is simply inconclusive. Tell you what, next week I’ll make some firm predictions on questions where I feel the data is incontrovertible. But the direction of the US economy is not yet clear. As I said in today’s blog, it’s changing … but it’s not yet clear. At least to me. Thanks again for your thoughts.

Terry