SHI 8/16/17: Cornucopia

SHI 8/9/17: Fact, Opinion or Fiction?

August 9, 2017

SHI 8/23/17: Nowcasting GDP

August 23, 2017

Of late, new economic data and “recession fears” have been ubiquitous.

PCE, CPI, oil, productivity, labor participation rates … the list of data updates goes on and on and on. Negative interest rates are back in the spotlight. And there is no shortage of recession talk, fear-focused on the frothiness of a 22,000 DOW and the aging of our current 8+ year economic expansion.

And finally, we have comments from Larry Summers, ex-US Treasury Secretary. No, not his Trump comments. But the FED concerns he shared in the London “Financial Times” over the weekend. We have a veritable cornucopia of data to review. Let’s dive in.

Welcome to this week’s Steak House Index update.

As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. At present, is the US economy expanding or contracting? We need to know.

The world’s GDP is about $76 trillion. At last count, our ‘current dollar’ US GDP is now over $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP — about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Recession talk is everywhere. Folks seem to feel it’s time for a recession.

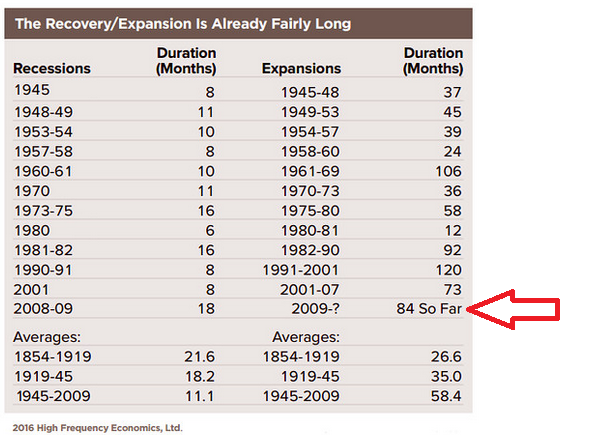

In prior blogs, I’ve shared my belief that economic expansions don’t die from old age. But there is no shortage of economics who seem to disagree. They post charts like this …

… and share their concern that the current expansion is “already fairly long.” And this chart is a year old!

Today, the duration of the recovery is about 96 months — and more people are expressing concern.

Maybe chatter alone will be sufficient to end this growth cycle. Especially when folks like Larry Summers, US Treasury Secretary under President Clinton and ex-Chief Economist for the World Bank, opine:

“If history is any guide, it is more likely than not that the economy will go into recession during the next Fed chair’s four-year term. Recovery is now in its ninth year with relatively slow underlying growth for demographic and technological reasons, very low unemployment and high asset prices. Even without these factors, experience teaches that recessions are almost never forecast or even rapidly recognized by the Fed or the professional consensus forecast, but there is at least a 20 per cent or so chance that if the economy is not in recession, it will be so within a year. So the likelihood that the next Fed chair will have to address a recession is probably about two-thirds.”

Perhaps. (Here’s a link to the article: https://www.ft.com/content/ad286162-7dd2-11e7-ab01-a13271d1ee9c)

Goldman Sachs has a slightly different view on the topic. Their financial model shows a 31% chance for a U.S. recession in the next nine quarters. And that there is now a two-thirds chance that the recovery will be the longest on record. “The likelihood that the expansion will break the prior record is consistent with our long-standing view that the combination of a deep recession and an initially slow recovery has set us up for an unusually long cycle,” they wrote.

Perhaps. I can say one thing with certainty, however: The popularity of this topic will continue to grow in the months and years ahead. You will hear and read the word recession a lot.

Is a recession mandatory? A certainty? Again, perhaps. But the timing, itself, is not. Nor is it predictable with any degree of certainty.

For example, when did China last experience a recession? In 1976 — over 40 years ago. No, I won’t argue the economies in China and the US have much similarity — other than the fact that today they represent the 1st and 2nd largest economies on the planet. Australia hasn’t seen a recession since 1991 – over 25 years ago. Australia’s expansion may soon surpass the duration of the Dutch expansion that kicked off in 1982, lasting for 103 quarters before succumbing to the 2008 global financial crisis.

My point? Take the media comments with a grain of salt.

But suppose a recession materializes? Would the FED use a rate cut to stimulate the economy? Can they?

In a recently published paper, Ken Rogoff, Harvard professor, commented the FED cut rates by an average of 5.5 percentage points in the nine recessions since the mid-1950s — an impossibility today without negative interest rates. A number of European central banks “went negative” in 2014, and the Japan central bank followed suit in 2016. This is certainly an option available to the FED. Perhaps not a desired option … but an option nonetheless.

Just recently, the quantity of bonds offering negative returns is growing again:

An interesting development to be sure. Take note: This $2 trillion increase is equal to 31%. That is large. Sure, it follows an equal decline the prior month … still, this is a huge increase, suggesting the desire for investment safety, once again, exceeds the value of ROI.

Essentially, this chart suggests a global bond-investor concern about an economic slowdown. So the jury is out … and a self-fulfilling prophesy could be in the making.

Let’s change gears … and take a quick tour of new economic data. We have a number of interesting recent data releases.

PCE: Personal consumption expenditures — just name for ‘consumer spending’ — is declining. This result is in close alignment with the SHI. Here is a 1-year chart, showing the most recent data, thru the end of June, courtesy of our friends at the St. Louis FED:

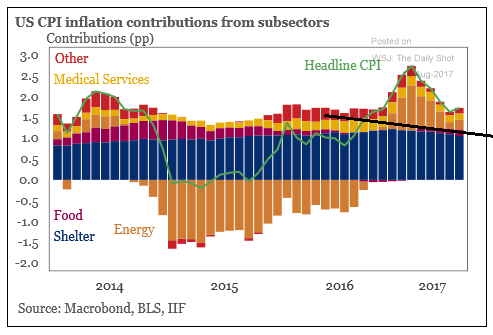

CPI: The more well-known, and more popular, inflation index — the CPI — continues to decline. Even this index is far below the FEDs 2% inflation target.

I really like the stacked bar chart below. Both ‘positive’ and ‘negative’ contributions to the CPI metric show for each month. The major contributors to the CPI — both up and down — show in various colors.

Take a look at ‘energy’ — the large brown bar. Between the middle of 2014 and 2016, energy cost was a huge drag on CPI, pulling the metric into negative territory during the second 1/2 of 2014. In the next few months I expect a similar move: energy will once again be a negative contributor to the CPI. Why? WTI futures are trading today at $47.87 per barrel, which is almost identical to the price one year ago, $46.58 on August 16, 2016. Yet, as you can see below, increased energy costs have lifted the CPI in the prior 9 months. This is likely to reverse in the next 6 or so months, resulting in a drag for the CPI. In spite of the OPEC production cap agreements, oil prices are right back to where they were one year ago.

Growing US supply continues to be the culprit. The International Energy Agency forecasts that global consumption will grow by 1.5 million barrels per day (bpd) in 2017 and another 1.4 million bpd in 2018. But, at the same time, US oil production is predicted to rise in 2017 by 800,000 bpd and another 1 million bpd in 2018, according to the US Energy Information Administration. Oil prices will fluctuate, but they are unlikely to increase meaningfully any time soon.

The black line is my addition. Notice it slopes from the high left to lower right. This highlights how the ‘shelter’ component of the CPI is finally slipping. Remember: rent (housing cost) is one of the largest components in the CPI calculation — a fact that’s easy to see by the size of the blue bar. After years of continuous annual rental rate increases, the trend has finally reversed:

Food, shelter, and energy costs — all major contributors to the CPI calculation — will remain flat or decline in the coming months. The FED will not find any inflation here.

Productivity: How about wage inflation? Nope.

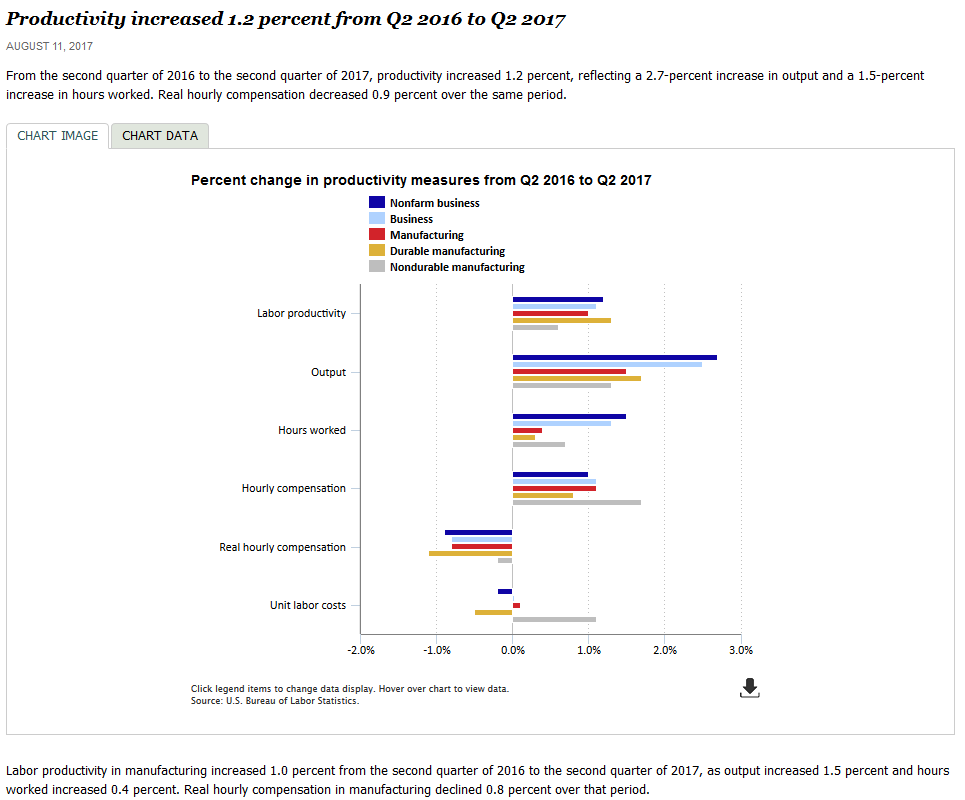

We’ve talked extensively on this topic in prior blogs — and now we have a bit of new data: Productivity. Per the BLS, we finally see a bit of improvement here — in the prior year, productivity increased by 1.2%:

According to my GDP calculation, productivity improvement plus growth in the US ‘civilian labor force’ (CLF) combine to form the top-end limiting factor for GDP growth. Between June of 2016 and June of 2017, the CLF increased by 1.256 million folks — to just over 160 million people — an increase of 0.79%. Added together, we have an upper limit on annual GDP growth of 1.99%. Right in line with my expectation and forecasts.

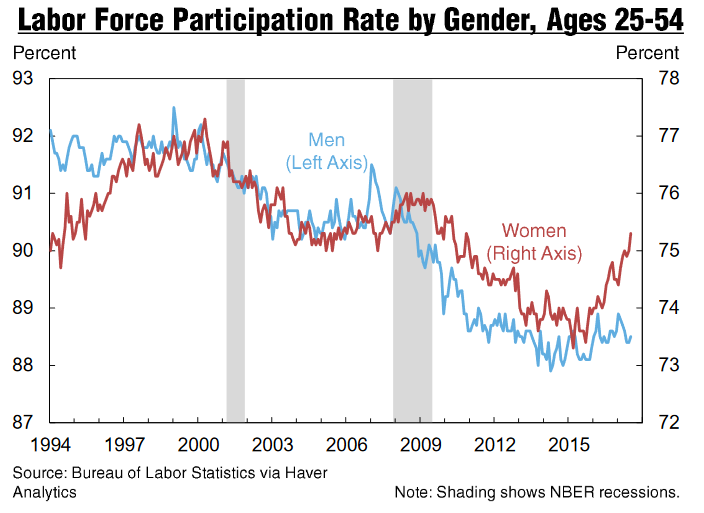

The US “labor force participation rate” peaked in the year 2000 – at 67.3%. (Recall the participation rate is the percentage of all US citizens — over the age of 16 and not institutionalized — who choose to work or look for a job.) Today, only 62.9% of our “civilian labor force” are working or seeking a job. But this doesn’t tell the whole story. Something very interesting is happening behind the numbers:

In the past year or so, fewer men are ‘participating’ in the labor force — and, at the same time, the number of women working or seeking jobs seems to be sky-rocketing. We’ll talk more about this in future blogs …. Now, it’s time to revisit our fancy steak houses.

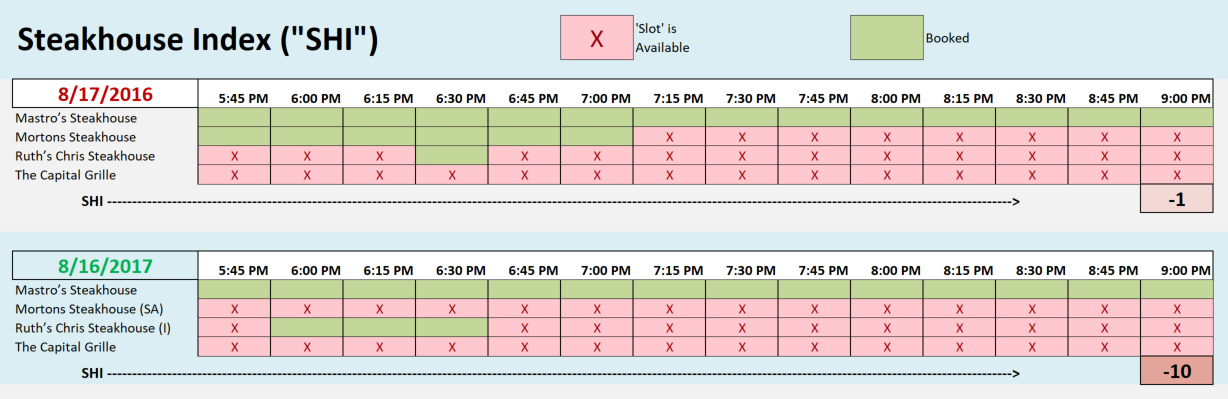

Well, the SHI remains subdued this week — today, 9 points below the same week last year — but this is a small improvement from recent weeks:

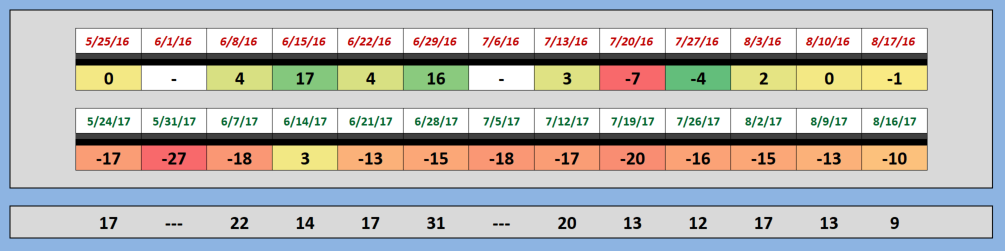

Mastros Ocean Club remains the perennial favorite, with Ruth’s Chris in distant second place. Mortons, once again, is completely available — a significant change from last year at this time. This slight improvement is not enough for me to change my opinion. It still reflects a weak state for consumer spending. I continue to expect a weak GDP growth rate in Q3. Here is the long-term trend chart:

As I said above, the 9-point difference between 8/17/16 and today’s SHI shows slight improvement. But the weak trend continues.

Let me finish today’s BLOG with a look the the FED minutes from their July meeting, released earlier today and a comment on “wildcard” political risk.

Here are a few choice excerpts from the FED minutes:

- “Total U.S. consumer prices, as measured by the PCE price index, increased 1-1/2 percent over the 12 months ending in May. Core PCE price inflation was also 1-1/2 percent over that same period. Over the 12 months ending in June, the consumer price index (CPI) rose 1-1/2 percent, while core CPI inflation was 1-3/4 percent.”

- “Despite their inter-meeting period gains, longer-term real and nominal Treasury yields remained very low by historical standards, apparently weighed down by accommodative monetary policies abroad and possibly by declines in the long-term neutral real interest rate over recent years.”

- “Many participants, however, saw some likelihood that inflation might remain below 2 percent for longer than they currently expected, and several indicated that the risks to the inflation outlook could be tilted to the downside.”

- “Participants discussed possible reasons for the coexistence of low inflation and low unemployment. These included a diminished responsiveness of prices to resource pressures, a lower natural rate of unemployment, the possibility that slack may be better measured by labor market indicators other than unemployment, lags in the reaction of nominal wage growth and inflation to labor market tightening, and restraints on pricing power from global developments and from innovations to business models spurred by advances in technology.

Here is their comment on the next FED rate increase: “Members agreed that the timing and size of future adjustments to the target range for the federal funds rate would depend on their assessment of realized and expected economic conditions relative to the Committee’s objectives of maximum employment and 2 percent inflation.”

And on the topic of reducing the FED balance sheet: “Although several participants were prepared to announce a starting date for the program at the current meeting, most preferred to defer that decision until an upcoming meeting while accumulating additional information on the economic outlook and developments potentially affecting financial markets.”

The bottom line? As I’ve suggested, the FED is in “wait and see” mode. They seem to disagree on direction … and a bit confused by current conditions. Confusion which clearly could have been avoided had they simply subscribed to my blog! 🙂

Political risk to US economic performance is rising. On one hand, we can’t ignore it. On the other, one has to ask how much impact this political risk might have on corporate profitability — profitability which, ultimately, drives stock market valuations. We’ll monitor this development as it occurs; for now, I simply wanted to mention it as a concern.

Combining and considering the market infatuation with recessing timing, the subdued economic metrics, the FEDs comments, and the political satire in DC, I remain convinced future GDP performance will be tepid. Q2 performance, I believe, will be solid, but Q3 and possibly Q4 are not looking robust.

- Terry Liebman

1 Comment

I value the article.Thanks Again. Keep writing.