SHI 9.16.20 – Let’s Talk About Debt

SHI 9.9.20 – Ask the Big Mac

September 9, 2020

SHI 9.23.20: Scarier than a Halloween Haunted House

September 23, 2020

Debt is like opinions — everyone has some, but these days they are reluctant to admit it. Household and sovereign debt levels are downright embarrassing. Collectively, they have never been larger. Embarrassing or not, let’s take a hike up the mountain.

” Climbing up Debt Mountain.”

Interestingly, all piles of debt are not the same. Some pay you interest. Others you pay to own. Odd? You bet.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion. No longer. It will shrink thanks to ‘The Great Lockdown.’ I did not coin this phrase — the IMF did. The same folks who track global GDP. Until recently, annual US GDP exceeded $21.7 trillion. Again, no longer. But what has not changed is the fact that together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Debt is a huge topic. Pun intended. 🙂

But so is the aggregate ‘household net worth’ of all Americans. Per the FEDs ‘Z.1’ report released in June, at the end of the first quarter of this year, household net worth eclipsed $110 trillion. Total assets of Americans, combined, exceeded $127 trillion … and total liabilities (debts) were about $17 trillion. Not bad, right?

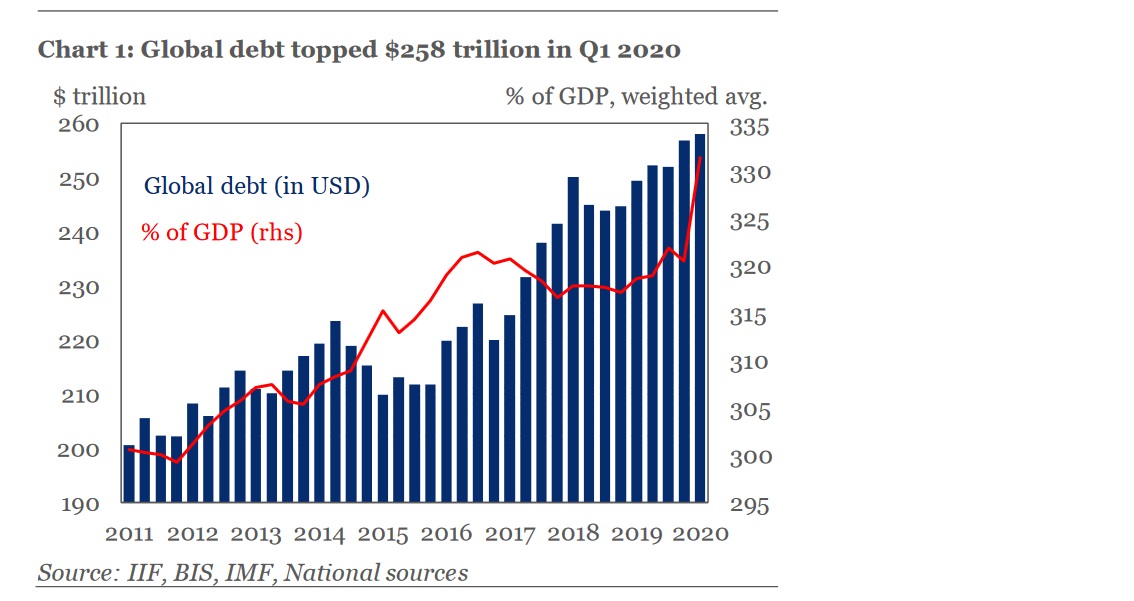

But the debt of American citizens is just the tip of the iceberg, so to speak. If we add up all debt across the globe, according to the Institute of International Finance, the mountain is much larger: $258 trillion at the end of Q1.

And the mountain continues to grow. In Q2 alone, issuance of new private and sovereign debt exceeded $8 trillion globally.

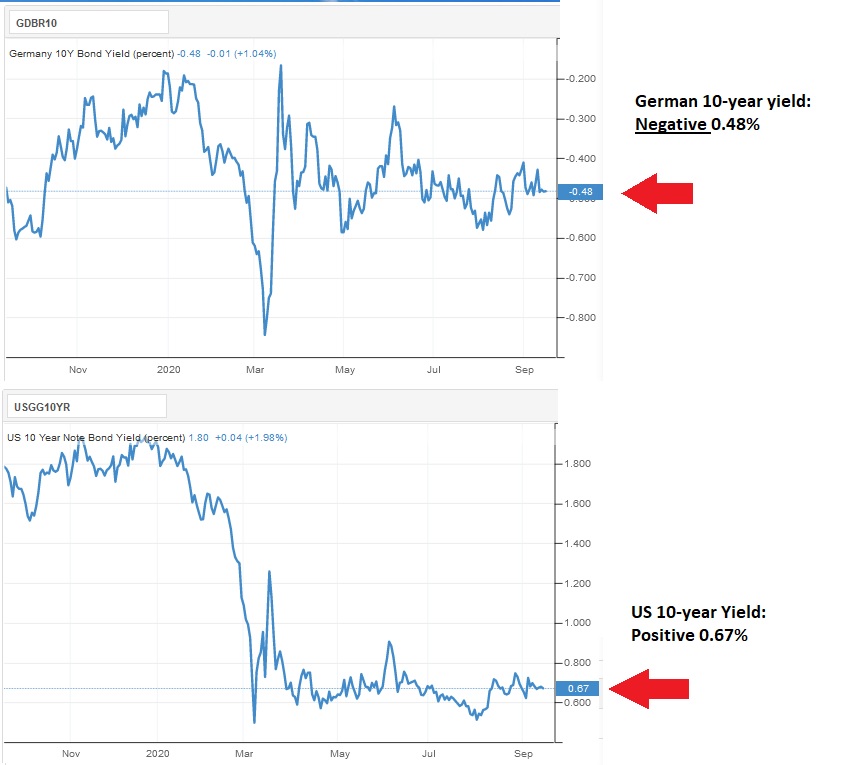

Debt is not all the same. Consider sovereign debts. As of this morning, the ‘yield’ on the German 10-year treasury was a negative 0.48 percent. Which means if you gave Germany $1 today, in ten years they would give you back about 95 cents. But here in the US, the 10-year treasury yields about 0.67 percent. So, using that same mythical dollar, after 10 years in a US security, the US Treasury would return about $1.07 to you. Much better! But still rather paltry. Here’s a 1-year chart of yields … one year ago, the yield on the 10-year UST was quite a bit higher:

And here’s the point: In my opinion, government debt in 2020 cannot be compared to government debt in 2000. Or 1990 … or 1980. They are not the same. Because interest rate levels have seen a structural shift, decade after decade, until now, where they are close to zero.

Don’t get me wrong: A mountain of debt can become impossible to handle … impossible to support. But that mountain is much smaller if the average treasury rate is 5% … and much larger if the average interest rate is 0.5%. And if the rate is negative? As it is in Germany? In theory, the bigger your mountain of debt, the better off you are! If Germany could borrow $1 trillion today, pay zero interest to the lender for 10-years, and then return $950 billion and be done, why wouldn’t they borrow trillions and trillions of euros?

Let me be clear: I am not advocating a willy-nilly, throw-caution-to-the-wind, massive debt binge. But I am suggesting that an intelligent, surgical, revenue-generating use of debt might be prudent where the long-term benefits far outweigh costs. The idea should be considered. By you … companies … and countries.

Clearly, we’re in uncharted waters here, folks. These conditions have never happened before. In the past, mountains of debt have always proven to be a problem. Always. Mountains of debt have caused countries to collapse. But in past years, that debt had a cost. Not today. Today a mountain of debt — at least for Germany — creates a net benefit for the country’s treasury. If Germany can borrow money at negative rates, and invest those funds in infrastructure or other income-producing assets, should they consider borrowing and investing more?

Perhaps. Again, we’re in uncharted water. And speaking of uncharted waters … the FED concluded their 2-day September meeting today. From the materials in their press release, we see their Federal funds rate forecast for the next few years:

- 2020: 0.1%

- 2021: 0.1%

- 2022: 0.1%

- 2023: 0.1%

In other words, at the present time, the FED expects to leave rates unchanged for more than 3 years. Once again, this has never happened before. So let me repeat that: Today, the FED reaffirmed they expect short term interest rates to remain near zero for more than 3 years.

Wow. Fed funds at zero for years. And a balance sheet of $7.01 trillion as of 9/10/20. That’s never happened before either.

2020. What a year. The year when the unbelievable becomes reality.

- Terry Liebman