SHI Update 7/5/17: A Shrinking World

SHI Update 6/28/17: Inflation? Where?

June 28, 2017

SHI Update 7/12/17: The Silent Giant

July 12, 2017

The US “total fertility rate” just declined again.

The CDC just released their report entitled “Births: Provisional Data for 2016.” You may be wondering why an economics and finance guy is talking about births. The reasons will become quite clear in the blog below.

Welcome to this week’s Steak House Index update.

As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/)

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. Is it expanding or contracting?

The world’s GDP is about $76 trillion. Our US GDP is almost $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early. Not when it’s too late.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

The nation’s total fertility rate, or TFR, may matter little to you today. But not to me. And by the time you finish today’s blog, I suspect you will have a much keener interest.

From a demographic perspective, I find it fascinating that our young people — in both the developed and developing world — are choosing to have fewer children. Perhaps as people moved from rural farm life into large cities, this outcome was inevitable: From a historic perspective, children have become very expensive. According to a USDA report out earlier this year, it will cost the typical, middle-income couple over $233,000 to raise one child from birth to age 17. No, this figure doesn’t include the cost of college. (The report did say families with 3+ children spent 24% less, on average, per child. Apparently, kids are cheaper by the dozen!) 🙂

Absent immigration, in years past a country needed a TFR of 2.10 to maintain a stable population. Above this figure, population will grow. Below, it will fall. Take a look at this graph courtesy of the World Bank:

First, note the data is thru 2014 — 2 years old. The 2014 TFRs shown above are:

- US: 1.86

- World: 2.45

- Japan: 1.42

- Iran: 1.71

Next, you’ll see I’ve added a line and this text on the image: “Replacement TFR: 2.10”. When a country’s TFR falls below the black line, its population (again, assuming no immigration) is actually shrinking year-over-year. Japan has been far below a 2.10 TFR for years. The US, too, has hovered at, or below, this level for decades. Our 2016 TFR is simply another dismal, declining reading, the lowest since 1984.

Now take a look at the World and Iran TFRs. Interesting, right? In the past 50 years or so, the globes total fertility rate has dropped in half. And the TFR in Iran has fallen so far, so fast it is quickly approaching the rate in Japan. Iran is disappearing before our eyes. Fascinating.

But the implications go far beyond a demographic curiosity. Over many decades, a below-replacement TFR can have a huge impact on a country’s finances — and even more dire, whether the country or its culture survives. But don’t take my word for it: Check out David Goldman’s new book entitled, “How Civilizations Die.” The author shares some rather chilling observations and predictions.

Permit me a quote from David’s book: “A decline in productive population accompanied by a rise in dependent retirees creates an economic tailspin, as the shareholders of U.S. auto companies and taxpayers of California and Illinois know well — and the residents of two dozen other American states are about the find out. Three-quarters of all Japanese and half of all Europeans will be elderly dependents by the middle of this century if the present low fertility rate continues.”

David’s point is simple. For generations, populations have grown consistently. It wasn’t that long ago the world’s greatest fear was over-population resulting in massive food shortages, suffering and starvation on a level never seen before. But about a generation or so ago, for some reason, things changed. Collectively, we began having fewer children. Go back to the graph above. In 1960, the total fertility rate in Iran was almost 7. Today its closer to 1.6 — far below the 2.10 TFR needed to maintain a stable population.

And now that the developed world has seen a hefty rise in “dependent retirees,” we have a problem: Without a sizable and growing young labor force, the US will have difficulty paying out retirement benefits. Because the system was designed many decades ago when TRFs were high and the population pyramid looked like, well, a pyramid. We used to have lots and lots of younger people at the bottom of that pyramid…fewer in ‘middle age,’ and very few old folks toward the top. But not today. Today our population pyramid looks more like a vertical cylinder. And in the decades to come it may begin to resemble an inverted pyramid.

In 2016, the US TFR fell once again to 1.81…down from 1.84 the prior year. This rate is well below the historic 2.10 “break even” fertility rate needed to keep our population stable. Now, one could argue — successfully, I believe — that we no longer need a 2.10 TFR to maintain a stable population. Life expectancy in 1960 was 69.7 years. Today, it is 78.8 years — a 13% increase.

But this doesn’t solve the problem; in fact, it exacerbates it. More people living longer lives means we have more dependent retirees than ever before. Think about this: In 1960, a man retiring at 65 received social security income and medicare for an average of 4.7 years before he passed away. Today’s retiree will receive those same benefits for 14.8 years — an almost 3X increase in duration! At the same time, with TFR remaining at all-time lows, fewer new workers are entering the labor force.

Which means that over longer periods of time, we run the risk of an insufficient labor force and shrinking tax revenues — both of which are needed to keep the economy healthy, GDP growing, and our retirees retired. Remember: The 6.2% of your income taken out of your paycheck for your “Social Security” savings account is not actually saved and set aside by the Treasury. It’s part of annual Treasury revenue. It is spent. Unlike your IRA or 401-K, where funds deposited are actually on deposit in your account, the Treasury uses today’s social security revenues to fund government operations. Retirement benefits payable today are paid from the “General Fund” and sourced from either current revenues or Treasury borrowings. There is no “retirement fund” where your social security money is deposited…there is no actual retirement account for you. Your social security benefits, when the time comes, will be paid from social security and income taxes paid by future labor.

You should be very worried by now. Absent a change in the US TFR or, alternatively, a change in how the US (and other developed nations) handle retirement benefits, we have some rough times ahead. At the minimum, we have some very tough decisions to make as a nation. Very tough.

Perhaps a steak will make us feel better. How are our “sophisticated, classic Steakhouses” with their “combination of world-class service and highly acclaimed cuisine” faring this week? Let’s take a look.

Hmmm…not too well. Once again, with the exception of Mastro’s every other ritzy steakhouse is wide open. Any table, any time, is yours for the picking:

Sorry, but once again we have no comparison week from last year. If memory serves me correctly, last year at this time I was in the Loire Valley at a friend’s daughter’s wedding … and, of course, tasting a few wines here and there. It was a lovely trip.

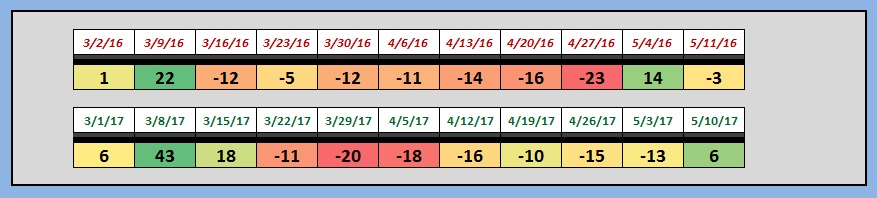

However, this week’s SHI reading of negative <-18> doesn’t require a comparative measure to assure you this is a very, very poor showing. And the longer term trend chart makes this even clearer:

Since 5/24 — with only one exception — our weekly SHI reading have been deeply negative. Again, with the exception of Mastro’s, no other steakhouse has any traction. We saw a similar trend early last year …

… but then the SHI turned positive and remained firmly in the green for months thereafter. Whereas this year, the SHI was quite weak from 3/22 thru 5/3, saw improvement for 2 weeks, then reservations fell off the cliff.

What does this mean? If the SHI is a meaningful barometer, and an effective proxy for consumer spending, it suggests US consumer spending is slowing. We’ve certainly seen this effect in auto sales. A couple of weeks ago, Bloomberg posted an article entitled, “Drop in U.S. Retail Sales Signals Uneven Consumer Spending” and commented,

“…retail sales fell in May by the most since the start of 2016, reflecting broad declines in categories including motor vehicles and electronics….”

Our SHI readings concur. It bears repeating that these signs indicate Q3 GDP may prove quite weak. Remember the definition of a recession is two consecutive calendar quarters with negative GDP growth. Reading the tea leaves and the SHI, I don’t think Q3 will be negative.

But the SHI and other indicators suggest second-half 2017 GDP is limping out of the gate.

- Terry Liebman

2 Comments

Very interesting. Keep ’em coming!

Awesome blog post. Really Great.