SHI 8.24.22 – From FOMO to FOOP

SHI 8.17.22 – Welcome to the Real World

August 17, 2022

SHI 8.31.22 – Supply and Demand for Steaks and Labor

August 31, 2022

We all know FOMO: “fear of missing out.”

There’s been plenty of that lately. Any FOMO we may have felt pre-pandemic before has only been exacerbated by recent events. What prospective homebuyer hasn’t experienced this feeling when their latest buying attempt in a multi-offer scenario fell flat? No deal! Yep, FOMO. FOMO has been rampant. Until now. Now we have FOOP. Do you know FOOP? That’s right: FOOP. It was a new one for me, too, and it envelopes nicely into this week’s blog.

“

Fear of missing out is so yesterday!”

“Fear of missing out is so yesterday!”

What is FOOP? Bear with me … I’ll get to that.

The CPI is a flawed yardstick. I don’t love it, but it’s pretty much the best we’ve got. Accurately measuring changes in the cost of living is difficult at best. Food, shelter and clothing are staples and necessities of modern life … and thus it is important to understand cost changes over time as best we can. Well, at least for food and shelter. Cheap clothing is quite easy to find – it just may not be fashionable. This may shock you, but I have shopped clothing in a “Thrift Store” once or twice. Take my word for it: there are some excellent clothing deals to be had in thrift stores… as long as you’re OK missing out on current fashion trends. ?

The CPI index, at least, is consistent in its methodology. Over longer periods, it does offer meaningful and actionable macro-data. For example, consider the cost of shelter – housing. Housing costs make up about 30% of the CPI index. As it should, right? We may be able to survive without the latest Channel outfit, but I think we’d all agree a roof over one’s head is important. Across time and the globe, from Anchorage to Abu Dhabi, from Zurich to Zimbabwe, having a place to call home is critical to us all.

Housing is important. Housing cost matters. Globally, housing cost is out of control.

And I believe the FED, and other central banks, are directly responsible for causing this problem. Now, they’re trying to fix their error.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Maybe. At the end of Q2, 2022, in ‘current-dollar’ terms, US annual economic output rose to $24.85 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 7.8%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

I now know why all the central banks across the developed world are raising interest rates in a coordinated, lock-step fashion. Well, of course, I don’t “know“ … but I think I do. See if you agree:

I believe the FED, and all the other central banks around the world, are looking for a “housing reset.” Yes, a housing reset. As discussed above, housing represents about 30% of the CPI, and about 1/3 of the typical household budget, in almost all countries across the globe. Housing is expensive. And it’s been growing more expensive, year after year, for almost a decade and a half. And it did the same in the decades preceding the Great Recession of 2008. But the past couple of years have been eye-popping. Home value increases have been absolutely staggering.

I believe that over the past 5 or 10 years, the FED, the ECB, the Bank of England, etc., directly and significantly contributed to the rapidly growing cost of a home or rent in almost every developed nation in the world. In fact, I believe the 65 central banker members of the Bank for International Settlements, or the BIS, have all (secretly) agreed they are responsible, to a great extent, for the fact that home prices, across the developed world, are out of control.

For years, I’ve ‘blogged’ about negative interest rates. Here are just a handful of my prior posts:

https://steakhouseindex.com/negative-interest-rates-really/

https://steakhouseindex.com/shi-8-6-19-staying-positive-in-a-negative-world/

https://steakhouseindex.com/shi-9-16-20-lets-talk-about-debt/

https://steakhouseindex.com/shi-3-3-21-staying-positive-in-a-negative-world/

Look at the date of the first post above: February 5th of 2016. That’s 2016 folks! And that’s not even when this exceptionally unusual chapter began … it began years earlier. I commented in the 2016 blog:

“The number of Central Banks sporting ‘negative’ interest rates is growing. First, in June of 2014, the ECB ‘pushed’ their ‘policy rate’ below zero. Months later, Sweden’s central bank followed suit. And then Switzerland…Denmark…Austria…Germany…and the Netherlands. And then, in a surprise move, Japan’s central bank jumped into the fray.”

That’s right … the ECB cut rates below zero back in 2014. Let me repeat that: Below zero. Over the years, many central banks in Europe followed suit, and others – like America’s Federal Reserve Bank – cut rates to zero, or very close. And then, for some seemingly inexplicable reason, many years later this happened:

Of course, I’m kidding. Inexplicable it was not. I would argue it was actually quite predictable. Ask yourself this:

Is it possible that exceptionally low interest rates, for an exceptionally long time,

helped propel home prices to record levels across the globe?

Is it possible?

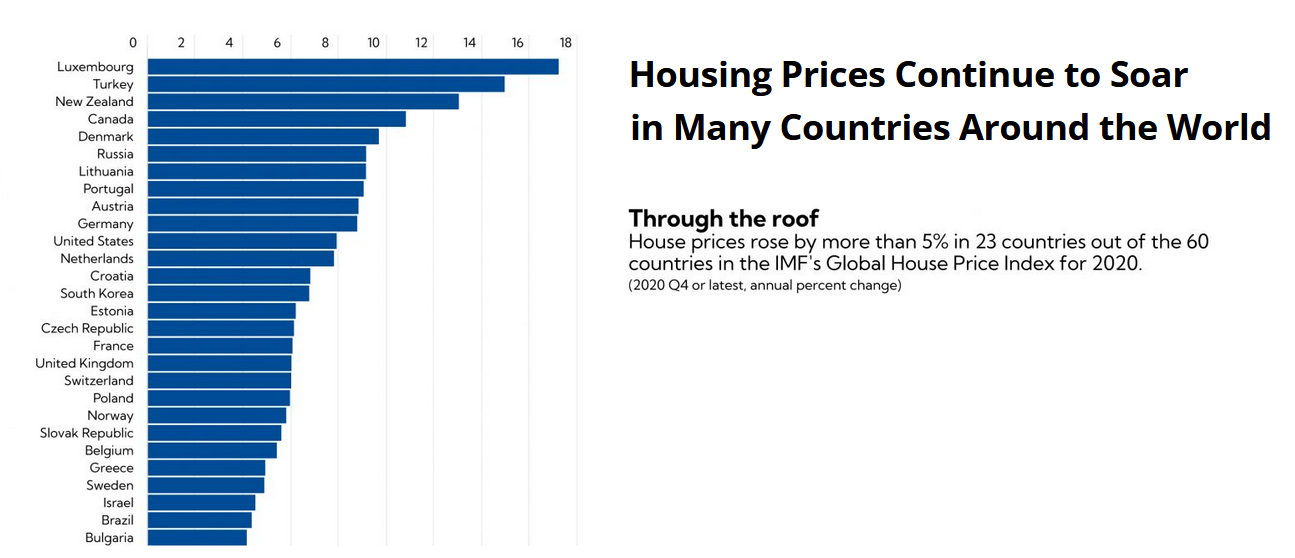

I clipped the data above from an International Monetary Fund (“IMF”) article published more than a year ago. It’s worth noting that the IMF sourced the data from the Bank for International Settlements — yes, the BIS — and the “World Economic Outlook.” It makes perfect sense the BIS has been tracking home value increases for decades. One must assume they have been alarmed by the growing body of data … but until now have done nothing about it. (Due to space limitations, I cropped the image, leaving off many other countries where home values were also quickly rising.)

Central banks around the world tell us today’s exceptionally high inflation rate is the reason they are lifting interest rates. It’s a smoke-screen. Sure, high inflation might be one of the many reasons behind almost every central bank’s move to raise rates now, but I think their primary objective is to stop run-away home value increases – the very problem the central banks created with their negative and zero rate policies.

On the corollary, I would also argue post-pandemic fiscal policy has also solved the chronic low-inflation mystery. The answer: Rain down a boatload of free money on your citizens and they will spend it, causing an “auction-mentality” spurring demand with static supply, pushing up prices and, ultimately, higher inflation across the board. Yep, MMT is dead … long live Monetarism!

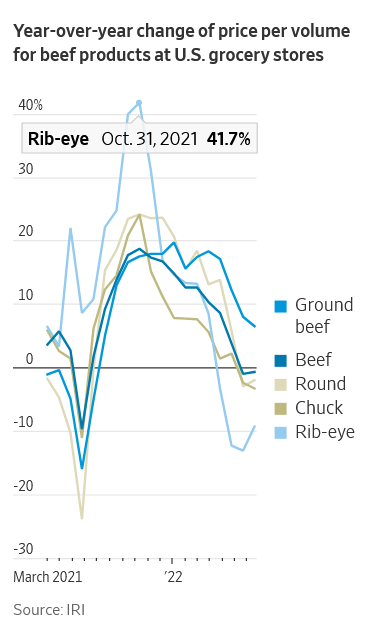

At the same time, it’s important to note that left to their own devices, capitalist market dynamics do ultimately work properly – if society and government permit them to work. For example, as this is the Steak House Index, I ask you to consider the price of a steak! In the recent past, prices were thru the roof — assuming you had a roof over your head in the first place 🙂

After peaking at a rib-eye popping, mouth-watering 41.7% increase at the end of October, 2021, Rib-eye prices have fallen significantly. In fact, as of August 7th of this year, the pound-price was down 9.3% from March of 2021. Take THAT, inflation! Why have steak prices fallen? Once again, it’s a supply/demand story: Softening consumer demand paired with better staffing at meat plants has effectively reduced demand while stabilizing/increasing supply. This is how unfettered, competitive markets work. When prices get too high, demand falls, production increases (assuming it can), and eventually the price falls again.

What goes up, can also go down.

And we’re back, full circle, to housing. Unfortunately, capitalist market dynamics don’t work well in housing. Land use restrictions and heavy-handed government regulation is excessive within this marketplace, preventing market dynamics from function properly. I blogged about this issue just a few months ago:

https://steakhouseindex.com/shi-4-20-22-regulation-nation/

Permit me to quote myself: “Regulations of all types have worked together to both reduce new home supply and increase new home cost — and this relationship is exceptionally dramatic in the past 10 years. Politicians across the country agree that home prices are too high … too un-affordable … and this is a serious American problem. But I don’t think I’ve heard even one politician place any portion of the blame on themselves. No, I’m not suggesting we should eliminate all regulation and let builders run amuck … that would be equally foolish. Reasonable, pragmatic constraints are needed. But the nature of these constraints should evolve over time as the needs of society evolve.”

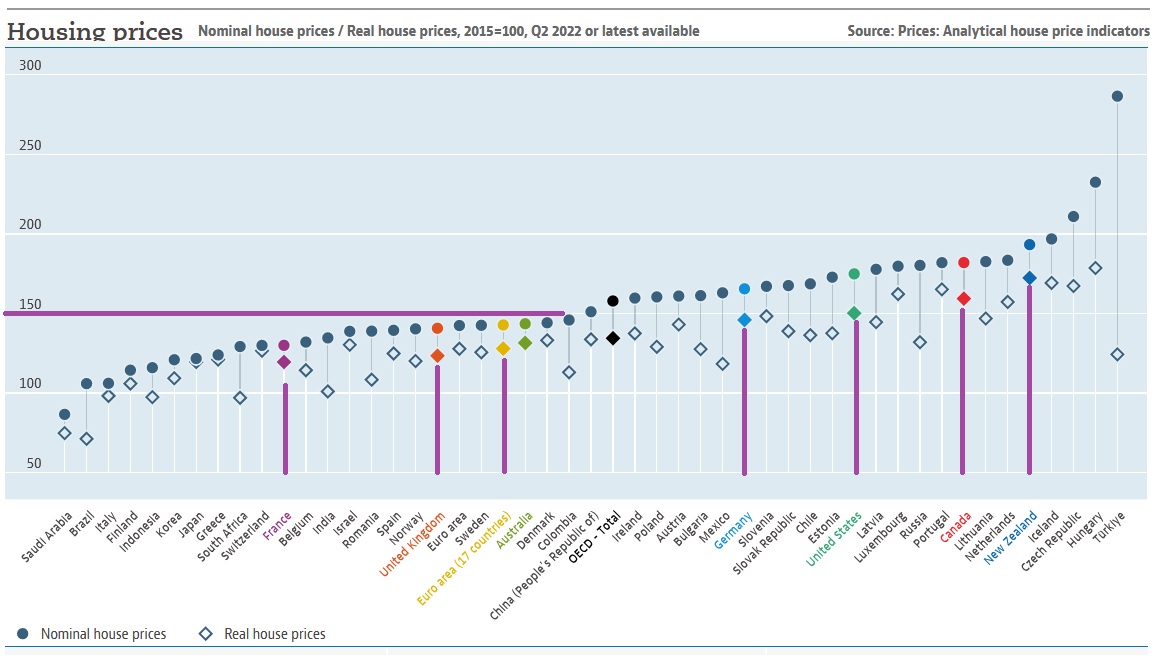

Central bank rate increases in both Canada and New Zealand have stopped home value increases in their tracks. Did you know home value increases in both markets have far surpassed those of the US during the same time? Take a look:

This chart, courtesy of the OECD, shows home price gains – since 2015 – across the globe. I highlighted certain countries in color – and further identified them with a vertical purple line. Finally, I highlighted the “150% appreciation” line in purple as well. The price gains shown by circles are the ‘nominal’ or current-dollar values. In other words, the price you would expect to pay. The diamond is the downwardly-adjusted, inflation-adjusted value. It’s interesting to see that only in very few countries – Brazil perhaps the most glaring – that the after-inflation-adjusted home value is negative.

Today, home values are falling in New Zealand. For the past 3 months, prices are down. The same is happening in Canada. The Royal Bank of Canada is a little concerned: According to a Canadian publication, the Financial Post, the RBC is fretting.

“Canada’s largest bank has downgraded its outlook for the housing market and now forecasts a “historic correction,” worse than any national decline seen in this country in the past 40 years. RBC sees home resales in British Columbia and Ontario falling 45% and 38% in 2022 and 2023, respectively, and prices falling more than 14% from quarterly peak to trough. The downturn will rival the decline Ontario saw in the early 1990s when sales fell 41% and prices 15%, but it’s not as bad as what B.C. went through in the early 1980s when sales fell 62% and prices 27%, said Hogue.”

Even though value increases in New Zealand and Canada surpassed those in the US, as we see in the chart above, the different is rather small. Thus, am I forecasting a general, market-wide home value drop here in the US too?

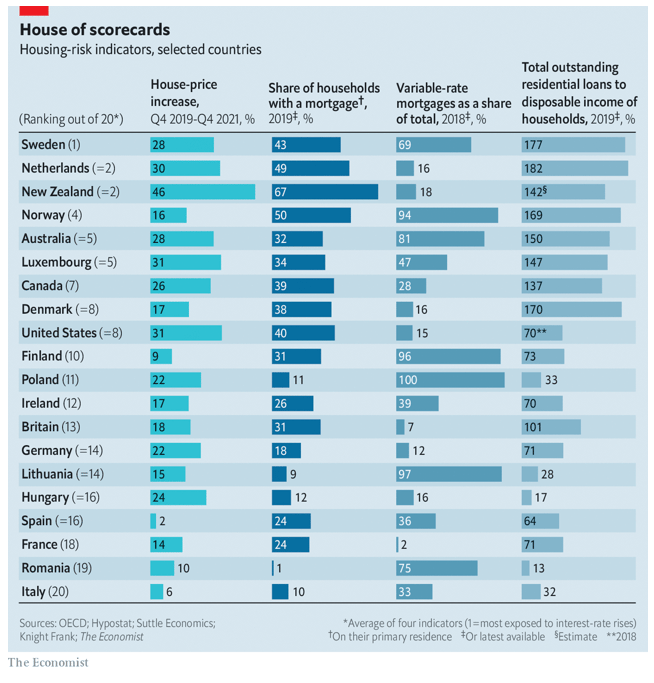

No. I am not. Why might home prices fall elsewhere but not here in the US you ask? Here’s why. Take a close look at the chart below:

While value increases are similar in size, there is one glaring difference between the US home-owners and those in Canada and New Zealand. Debt ratios. People in both countries have crazy-high household debt ratios. Their citizens were struggling to manage their housing costs before the rate increases. On the other hand, at least the majority of their home loans are fixed interest rates. Just as we have here in the US. In New Zealand, only about 18% of all home loans are variable rates. The other 82% are fixed. In Canada, the figures are only slightly worse: 72% of all home loans are fixed.

And then we have Australia. Ouch. Only about 19% of Australia’s home loans are fixed rates. And their debt ratios in 2019 were already sky high at 150% of disposable income (see chart above).

Meaning that the month after the Bank of Australia raises their short-term interest rate from around zero to about 1.85%, monthly mortgage payments quickly increased too. According to TradingEconomics, the Australian mortgage rate increased to 6.14% in July. This may not seem too bad … but keep in mind that interest on a $1 million loan at 2% costs about $20,000 per year; at 6%, that same loan costs $60,000 per year. And many fear rates and payments will go higher still.

So they are waiting. Sitting on the sidelines. FOMO is gone … and FOOP is here. FOOP: Fear of Over Paying.

Meanwhile, back in Canada, the RBC doesn’t believe the housing market will collapse. Instead, sources suggest they see the sales and price downturn as a “welcome cooldown” after a …

“… two-year buying frenzy that put home-ownership out of reach for many Canadians.”

Here’s the recipe for a frenzy: Have all your central banks ushered in super low and negative interest rates for almost a decade. Add a pandemic. Lower rates even more. Add a dash of salt, a pad of butter, and a boatload of cash, stir vigorously, and … BAM! You have run-away home prices! And inflation! 🙂

And so, today, the central bank members of the BIS are trying to put the proverbial “genie-back-in-the-bottle.” By raising short term rates and ending ‘quantitative easing,’ they are directly targeting home mortgage rates. In ‘fixed-rate’ markets with lower DTI ratios — like here in the US — home values will respond slower. Countries with neither may be in trouble. Time will tell.

Of course, value increase will definitely slow significantly here in the US as we’ve seen already … and some markets may even experience value losses. This is the result the FED intended. However, in highly variable home loan markets — like Australia and Norway — home values will react far more swiftly and inversely to the size of the rate hikes … the higher the rates go, the greater the pressure on home values, and potentially, the greater the losses in home value. As rates rise, sales activity will slow, putting further pressure on home prices. A classic negative-feedback loop has begun around the globe, thanks to our friends at the BIS.

A good thing? Bad thing? Like with all things in life, it all depends on your personal perspective and point of view. I’ll leave that conclusion to you.

FOMO is gone … long live FOOP!

FOOP: The fear of over-paying. I rest my case. To the steak houses!

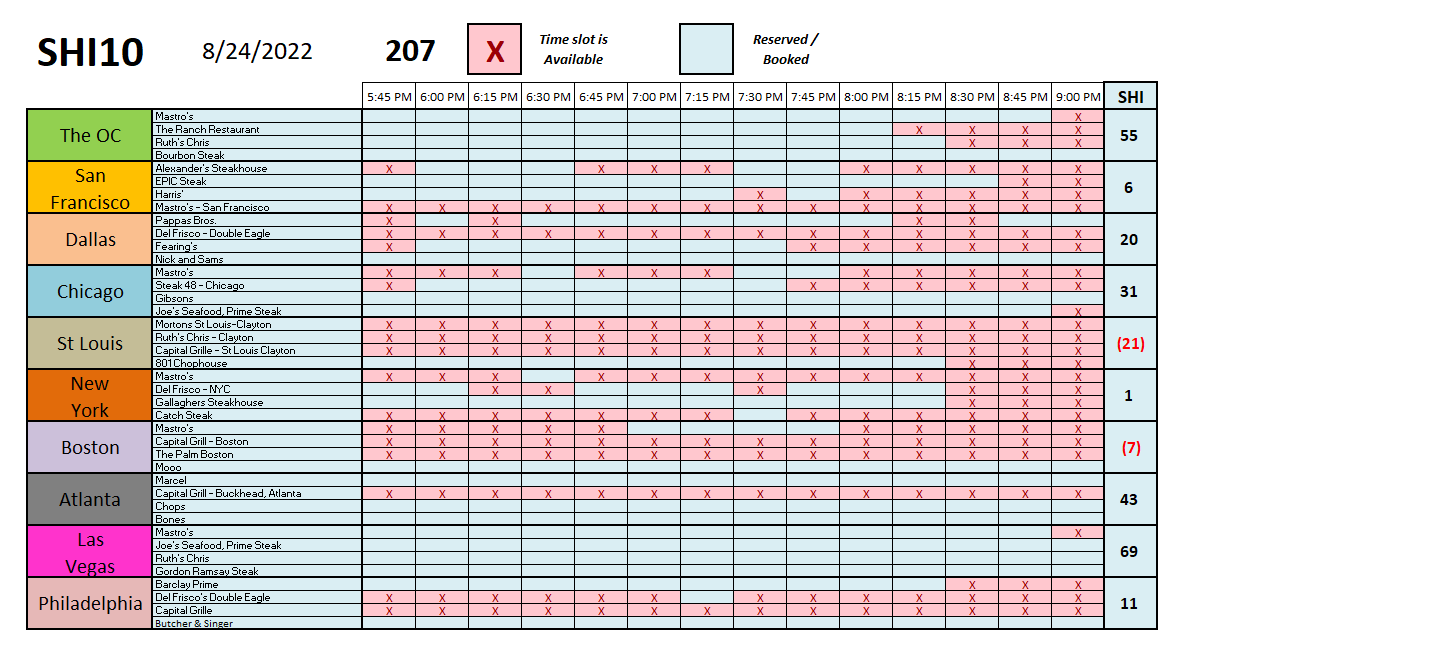

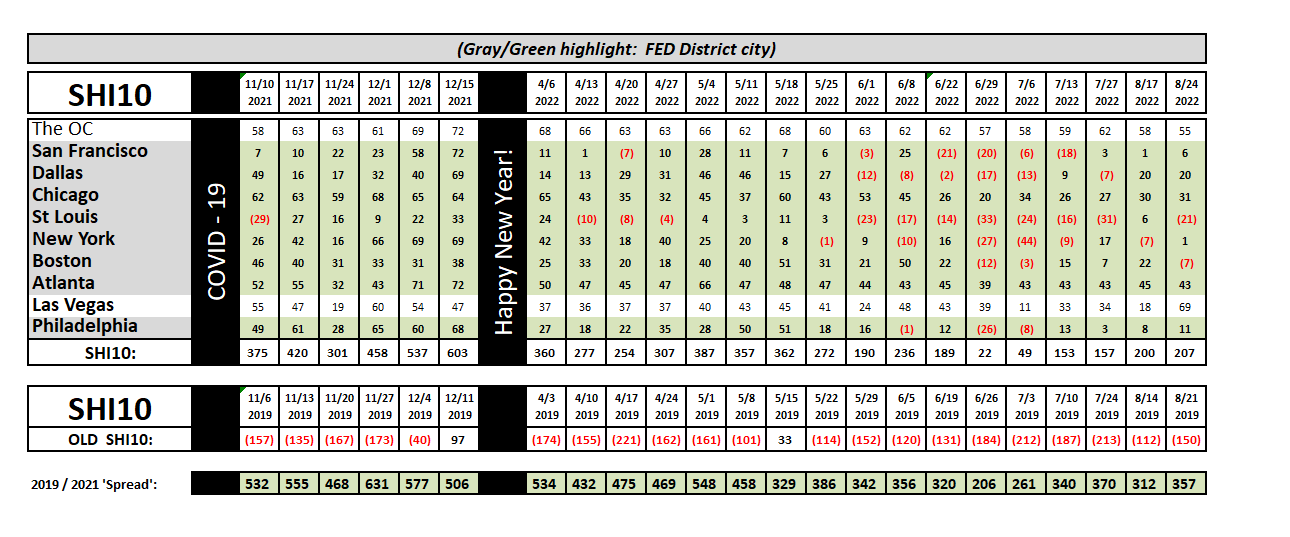

Interesting. The SHI40 reading is consistent with last week … but we see a lot of movement in the individual cities. Check out ‘Vegas: The expensive eateries are almost completely booked this Saturday! And St Louis is almost completely available. Here’s the trend report:

Expensive steak house reservation demand remains strong. By my metric, folks, the economy is chugging along just fine. Of course, don’t ask a mortgage or real estate broker if he/she/they agree. They may have to sell their Ferarri to scrap up the cash for next month’s mortgage payment. 🙂

<:> Terry Liebman