SHI 8.5.20 – Is an Inflation Wave Heading our Way?

SHI 7.29.20 – Did Someone Mention Gold?

July 29, 2020

SHI 8.12.20 – Not Thinking About Thinking

August 12, 2020

No. I don’t think so. At least not consumer price inflation. The flood of fiscal and QE stimulus notwithstanding, I remain unconvinced the US will experience an inflation spike any time soon. No, in the near term, I’m more concerned about deflation. And over time, as our economy heals, I believe consumer price inflation will remain quite tame.

Alternatively, as I said in last week’s blog, I believe the world is likely to see significant asset value increases over the next few years; but, this notwithstanding, I feel consumer inflation will remain flat. Rest assured, plenty of people disagree with me. And since so many disagree, you must ask this question:

” Why take my word for it? “

Perhaps you shouldn’t. All forecasts are dodgy at best. Predicting the future is inherently risky. But if you do decide to listen to someone’s prediction, consider the source. How accurate has it been in the past? Great question. I’ve made numerous forecasts over the years. Even better: My forecasts have all been in writing so we can go back and check! Have I been right more than wrong? Let’s find out … join me on a trip down memory lane.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion today. No longer. It will shrink thanks to ‘The Great Lockdown.’ I did not coin this phrase — the IMF did. The same folks who track global GDP. Until recently, annual US GDP exceeded $21.7 trillion. Again, no longer. But what has not changed is the fact that together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Have my predictions been generally accurate? Let’s take a look:

- SHI 08.31.16: I said, “I feel the FED will raise the FED funds rate once this year. My guess: In December. By 1/4%.” They did. They raised rates by 1/4% … and they did it in December of 2016. Nailed it. https://steakhouseindex.com/steak-house-index-update-83116/

- SHI 6.26.17: I asked the questions, “Inflation? Where?” And I opined that the Philips Curve was dead … and inflation would remain low. It did. https://steakhouseindex.com/shi-update-62817-inflation-where/

- SHI 09.19.18: I stated, “The next recession will begin within 2 years.” It did. We are in it. https://steakhouseindex.com/shi-09-19-18-one-thing-is-certain/

- SHI 9.4.19: I opined, “I believe US interest rates will generally remain positive.” They have … and the FED is committed to keeping US rates from going negative. They expect rates to remain exceptionally low, effectively at zero, but not negative. https://steakhouseindex.com/shi-9-4-19-global-government-debt/

I could go on and on. I feel good about my record and prediction accuracy. And since we’re on the topic of interest rates, I have consistently predicted long-term rates would decline, even as other financial luminaries, such as the CEO of JPM Chase, Jamie Dimon, predicted the opposite would happen. In fact, in August of 2018, Mr. Dimon was quoted as suggesting the 10-year Treasury could hit 5%. “It’s a higher probability that most people think,” he opined. I disagreed then … and in my blogs repeatedly commented I felt US rates were likely to follow the rates of other developed nations: DOWN. Way down. Not up, as Mr. Diamon believed and projected.

And today the 10-year US Treasury is closer to 0.50% than 5.00%. Clearly I was right and Mr. Diamon, wrong. Of course, neither of us expected the pandemic … which is responsible for today’s exceptionally low interest rates. But my prediction would have been accurate without the pandemic. And Mr. Diamon, once again, was wrong. What’s my point?

Simply this: The ‘prediction business’ is inherently risky. If the pandemic has taught us one thing, it’s that the future is clearly unwritten. And unpredictable. The challenge, of course, is this: if you’re attempting to make some sense out of the economic soup all around us, and figure out how to navigate current and near-term conditions, you must engage in a bit of fortune-telling. You must. And since you have to do it anyway, you should seek out the opinions of people who have been more right than wrong. People like me. 🙂

On the other hand, if you ask my wife, I suspect she’d say I’m generally wrong. What can I say? I’m a guy. In fact, in my most recent ‘father of the bride’ speech, I used a well-worn quip on this exact topic when offering my new son-in-law a bit of exceptionally good advice:

“Son, welcome to the family,” I said, “Now that you’re married, you will quickly discover that you and your new bride — my beautiful daughter — will encounter some challenges, and you may disagree about how to resolve them. Let me assure you of one thing. Now that you are married, when you encounter this first disagreement with your new bride, keep in mind there’s an easy way to know who right and who is wrong: Always remember that one person is always right and the other person is always the husband.”

OK, it was intended to be a joke. Or was it? Yes, it is only a joke. Seriously. 🙂

So why do I believe US inflation will remain tame in spite of the MASSIVE global QE and fiscal stimulus … and with more coming soon here in the US? It’s a great question, worthy of a great debate. At present, if I remain steadfast in my believe that US consumer inflation will remain tame for two primary reasons.

First, the ubiquitous US dollar. Earlier this week, the Wall Street Journal published an article entitled, “Covid Supercharges Federal Reserve as Backup Lender to the World.” Indeed.

Across the globe, the FED has telegraphed a crytal-clear message: The FED will backstop US and global dollar. As needed. During Q2 of this year, the FED lent close to half a trillion of US dollars to the Bank of Japan, the ECB, the Bank of England and other central banks around the globe. And this was after they purchased another $1/2 trillion of Treasuries from fearful investors spooked by the pandemic. Both moves, nearly $1 trillion in total, helped ease a global dollar shortage and keep financial markets functioning correctly.

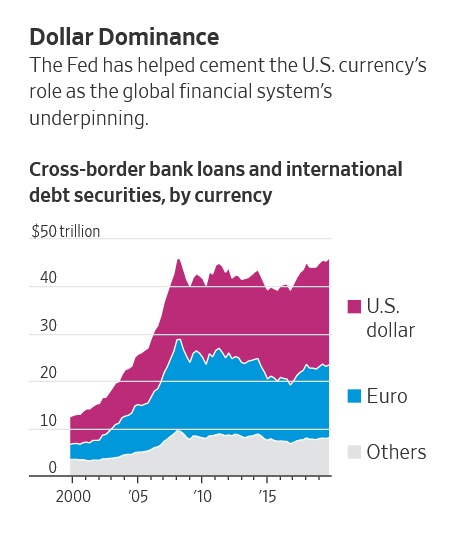

The rise of China’s economic power notwithstanding, the US dollar remains the world’s currency. The Bank for International Settlements (BIS), the central bank for central bankers, tracks the amazing prominence of the dollar. Consider this fact: Some 88% of the $6.6 trillion in currency trades that take place on average daily involve dollars. Yes, you read that correctly. I’ll repeat: $6.6 trillion every day.

Take a look at the chart to the right. According to the WSJ, as of the end of 2019, “the volume of U.S. dollar-denominated international debt securities and cross-border loans reached $22.6 trillion, up from $16.5 trillion a decade earlier, according to BIS data.” Dollar use around the world is growing, not shrinking, no matter what you might hear from the media.

About 1/2 of all “cross-border” bank loans and debt securities are made in dollars. This in spite of the fact that there are about 195 countries in total, still about 1/2 of all cross-border debts are US dollar based:

- US Dollar: $22.58 trillion

- Euro: $15.44 trillion

- Other: $7.97 trillion

The dollar’s hegemony makes other countries unhappy. China, of course, being the most unhappy. I have no doubt the ECB and China will continue to attempt to erode the dollar’s role in global debt transactions, but I doubt they will have much success. Why?

Think of it this way: Imagine you’ve built and own a massive, super-highway that spans the globe. Cars zip along at high speeds over this highway, above buildings, rivers, oceans and mountain peaks. It’s a great highway … enjoyed by all. Of course, it’s not a free highway. It’s a toll road. Each user must make a 1- to 30-year commitment to use the toll road before their first trip. But the cost is reasonable and the convenience is undeniable. Time passes. Along comes your neighbor. He’s not happy using your toll road. He want’s to build a competing highway system. But, alas, he cannot, because he lacks the resources, capital and most importantly, the willingness of the drivers to switch road systems, to a great extent because of the long-term commitments made years ago. Sure, your neighbor might be successful over time, but any success will not be realized for years or decades.

Thus, the US dollar remains the behemoth it is. Here’s the WSJ article if you’re interested:

Why is the dollar’s global standing important in this context? Because while the US has an “official” money supply count, as we’ll discuss below, the true US dollar money supply is probably impossible to calculate, due to number of non-US transactions in dollars. The dollar is truly the world’s currency. This is a fact. Which means the traditional conceptual economic relationship between the “supply” of currency and the “demand” for goods and services in the Keynesian economic model breaks down. It just doesn’t work under these conditions, inasmuch as the “system” is not closed or constrained within the borders of the United States. Currency excesses, to the extend they exist, are simply absorbed into the global financial system.

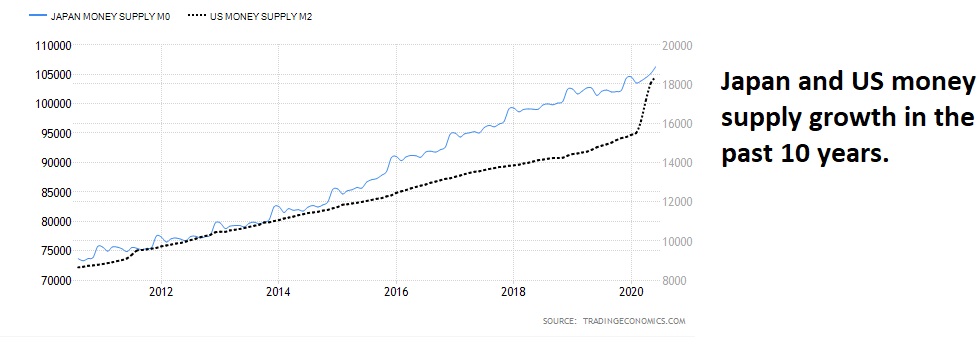

Which brings us to ‘reason #2.’ Another prominent country, one very similar to the US in many respects including demographics, has unsuccessfully tried to “inflate” itself using currency growth and debt. Of course, I’m talking about Japan. Japan shows us a likely future for the US.

As you can see below, money supply growth in Japan has been on a tear for years. (Japan: Blue line. The US is the black dotted line.) In spite of Japan’s almost moribund and near-absent GDP growth, their money supply has steadily increased — much faster than our domestic ‘M2’ money supply. Our US GDP growth, while slower than decades past, has consistently beat Japanese GDP growth by a wide margin — yet our M2 supply has grown much more slowly. That is, until 2020 when the printing presses began to work 24/7 after “The Great Shutdown.”

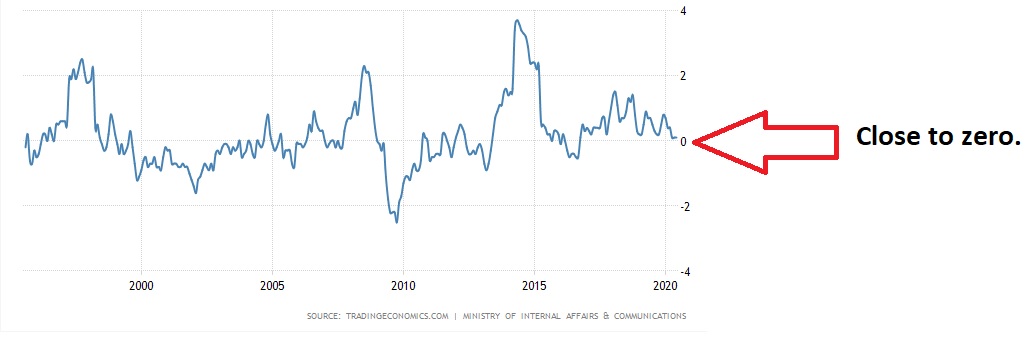

For decades now — I’ll repeat: DECADES — Japan has been trying to ‘juice up’ the inflation rate without success. Their money supply has expanded at unprecedented rates, government borrowing exceeds all other countries by a factor of about 2X, but inflation growth has remained muted. Below is a 25 year chart of consumer inflation in Japan. Sure, they inspired a brief inflation spike back in the late ’90s, and once again about 6-7 years ago, but consumer inflation has hovered very near zero much of the time. In fact, during much of this period, Japan has experienced serious bouts of deflation.

Japan’s currency is strong and well respected. But the yen is primarily used within the country. Thus, the traditional Keynesian economic principals should apply here. If the production of goods and services are relatively consistent (GDP), but money supply is growing rapidly, interest rates should rise and inflation should spike. But their interest rates remain close to zero just like their inflation rates. Demographics, something Keynes never modeled, plays a large role here. But that’s another discussion for another day.

For these reasons, I doubt the US will see much consumer inflation. Yet I’ve stated I believe the US and the world will experience asset value inflation. Which begs this question: Can the US experience significant asset inflation without concurrently experiencing runaway consumer price inflation? I believe the answer is yes, but we’ll save this discussion for another time.

– Terry Liebman